CSS Essay Outline

- Introduction: poverty alleviation through collective economic power

- Thesis statement

- Meaning of cooperative societies

- Meaning of poverty alleviation

- Philosophical basis of cooperation: self-help, mutual aid and democratic ownership

- Historical origin of cooperatives in South Asia

- Cooperative Credit Societies Act, 1904 and its purpose

- Evolution of cooperative movement in Pakistan

- Legal framework: Cooperative Societies Act, 1925

- Pakistan’s poverty challenge in the contemporary economy

- Rural poverty and the vulnerability of small farmers

- Agriculture, livestock and rural livelihoods in Pakistan

- Why individual poor households remain weak in markets

- Cooperatives as institutions of collective bargaining

- Cooperative credit and protection from informal moneylenders

- Input cooperatives and reduction of production costs

- Marketing cooperatives and better prices for small producers

- Dairy and livestock cooperatives as poverty-reduction tools

- Women’s cooperatives and household income

- Youth employment through modern cooperative enterprises

- Cooperatives and food security

- Cooperatives and climate resilience

- Water-user cooperatives and irrigation management

- Housing cooperatives and urban poor

- Savings cooperatives and rural financial inclusion

- Successful international model: Amul and dairy transformation

- Global recognition: UN International Year of Cooperatives 2025

- Cooperatives and Sustainable Development Goals

- Punjab’s cooperative sector: scale and potential

- Why cooperatives in Pakistan have underperformed

- Elite capture, politicization and weak audits

- Lack of professional management and digital systems

- Cooperative frauds and loss of public trust

- Counterargument: cooperatives often fail and markets are more efficient

- Response: failure lies in governance, not in cooperative principle

- Need for cooperative revival in Pakistan

- Reform agenda: law, transparency, digitalization and professional management

- Cooperatives for Pakistan’s poverty-reduction strategy

- Book references and intellectual support for cooperative development

- Conclusion: cooperation as a path from dependency to dignity

Essay

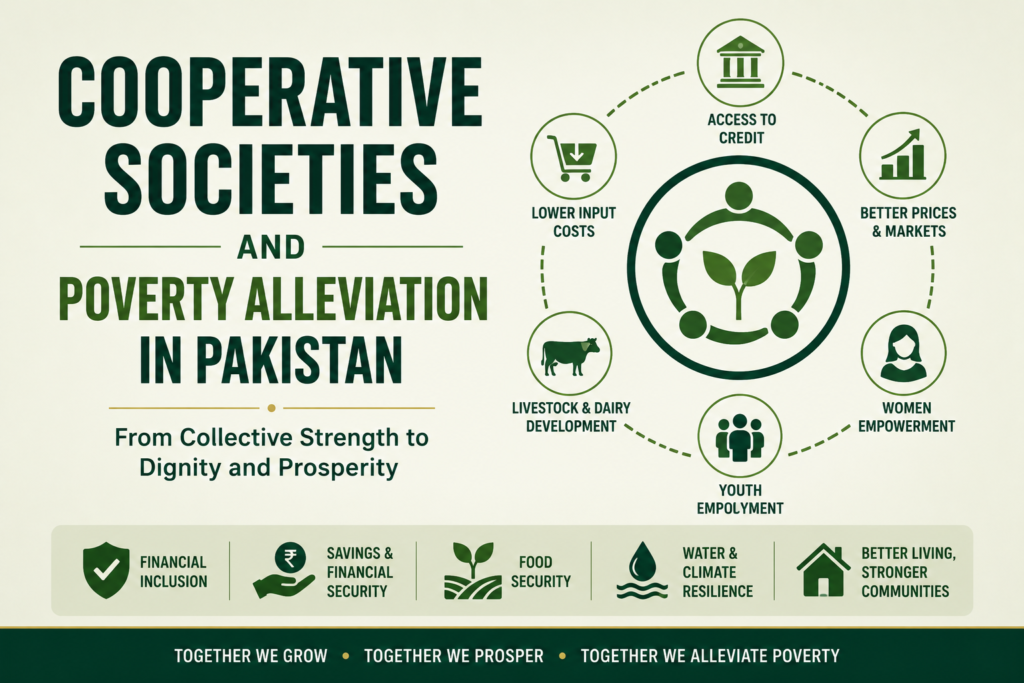

Poverty is not only the absence of income. It is the absence of power. A poor farmer may have land but no bargaining power. A rural woman may have skills but no market access. A milk producer may own livestock but no cold chain. A tenant may work hard but remain trapped in debt. A small shopkeeper may earn daily but remain outside formal finance. In such conditions, poverty cannot be removed by charity alone. It requires institutions that convert scattered weakness into collective strength. Cooperative societies are among the most important of such institutions.

A cooperative society is a voluntary association of people who unite to meet common economic, social or cultural needs through a jointly owned and democratically controlled enterprise. It is based on self-help, mutual aid, democratic decision-making, economic participation and concern for community. Unlike private companies, cooperatives are not created merely to maximize profit for outside shareholders. Unlike government departments, they are not supposed to be controlled by bureaucracy. Their members are both owners and users. This makes them particularly suitable for poor and rural communities, where individual households lack capital, technology, information and bargaining power.

The thesis of this essay is that cooperative societies can become powerful instruments of poverty alleviation in Pakistan by expanding access to credit, inputs, markets, livestock services, savings, women’s enterprise, youth employment, food security and climate resilience. However, their impact has remained limited because of politicization, elite capture, poor audits, weak regulation, lack of professional management, low public awareness and loss of trust. Pakistan needs a modern cooperative revival based on transparent governance, digital records, inclusive membership, financial discipline, professional management and strong regulatory oversight.

The philosophy of cooperation is simple: people who are weak individually can become strong collectively. Cooperation does not deny individual effort; rather, it multiplies it. A single farmer cannot buy fertilizer at wholesale price, hire modern machinery or negotiate with large buyers. But a group of farmers can. A single woman may not be able to sell handicrafts beyond her village, but a women’s cooperative can create a brand, arrange transport and use digital markets. A single milk producer cannot build a chilling plant, but a dairy cooperative can. Thus, cooperation is not a slogan. It is an economic method of empowerment.

Historically, the cooperative movement in South Asia began under colonial rule as a response to rural debt and moneylender exploitation. The Punjab Cooperatives Department records that the movement was introduced by the British government through the Cooperative Credit Societies Act, 1904, mainly to rescue agriculturists from exploitative credit systems. A State Bank of Pakistan historical chapter similarly notes that the cooperative movement started in British India with the Cooperative Credit Societies Act, 1904, whose objective was to provide agricultural credit to small farmers at low interest on a self-help basis. This historical origin is important because the original purpose of cooperatives was poverty alleviation through affordable credit.

The movement later expanded through the All India Cooperative Societies Act, 1912, and after independence Pakistan inherited the cooperative legal and institutional framework. The Cooperative Societies Act, 1925 remains one of the foundational laws for cooperative regulation in Punjab and other areas, with provincial amendments and rules. The Punjab Cooperatives Department still describes cooperatives as autonomous associations of persons voluntarily united to meet common economic, social and cultural needs through jointly owned and democratically controlled enterprises. Therefore, cooperatives are legally and historically rooted in Pakistan’s rural development tradition.

Pakistan’s current poverty challenge makes cooperatives highly relevant again. The World Bank reported in 2025 that Pakistan’s earlier poverty reduction had reversed because of economic shocks, weak structural reforms, inflation, COVID-19 impacts, global price pressures and the devastating floods of 2022 and 2025. Reuters, citing World Bank findings, reported that poverty had declined from 64 percent in 2001 to 22 percent by 2019, but rose again to about 25 percent by 2024. A World Bank blog also stated that an additional 13 million Pakistanis were pushed into poverty, bringing the projected poverty rate to 25.3 percent by 2023–24. These figures show that millions remain vulnerable to shocks.

The situation becomes more serious when measured through wider poverty lines. Pakistan’s Poverty and Equity Brief, as reported in 2025, estimated poverty at 42.4 percent in FY2025 under the lower-middle-income poverty line, with population growth adding pressure. The World Bank’s April 2025 Pakistan Development Update projected poverty at around 25.6 percent in FY25 under the national line and warned that weak growth was insufficient to reduce poverty. These different figures reflect different poverty definitions, but the conclusion is the same: Pakistan faces a serious poverty challenge, especially among households exposed to inflation, weak jobs and climate shocks.

Rural poverty is particularly important because Pakistan remains a largely rural and agriculture-linked society. World Bank data show that a majority of Pakistan’s population still lives in rural areas. Agriculture remains central to rural livelihoods. The Pakistan Economic Survey 2024–25 reported that livestock contributed 63.6 percent to agriculture and 14.97 percent to GDP, growing by 4.72 percent in FY2025. At the same time, agriculture sector growth was only 0.56 percent in FY2024–25, showing pressure on rural production and income. When agriculture slows, rural poverty worsens because millions depend directly or indirectly on farming, livestock, labour and local rural markets.

The poor are weak in markets because they are fragmented. A small farmer buys inputs at retail price and sells produce at distress price. A landless labourer has no savings and no insurance. A livestock-owning woman sells milk through middlemen because she lacks chilling facilities. A small artisan cannot access urban customers. A poor household borrows from informal lenders because banks demand documentation and collateral. This fragmentation is the economic root of poverty. Cooperatives address it by organizing the poor as a collective economic unit.

The first major contribution of cooperatives to poverty alleviation is access to credit. Rural poverty often deepens because poor households borrow at high cost from informal moneylenders, input dealers or commission agents. Such credit is not merely expensive; it creates dependency. A farmer who borrows for seeds may be forced to sell his crop to the same lender at a lower price. A cooperative credit society can reduce this exploitation by mobilizing local savings, providing loans at reasonable rates, assessing borrowers through community knowledge and ensuring repayment through mutual accountability. This was the original purpose of the cooperative movement in South Asia.

The second contribution is access to agricultural inputs. Seeds, fertilizer, pesticides, diesel, electricity, animal feed and machinery services are expensive. Small farmers often buy them late, in small quantities and at high prices. Cooperative input societies can purchase in bulk and distribute to members at lower cost. They can also help prevent fake seeds, adulterated pesticides and poor-quality fertilizers by dealing with certified suppliers. Lower input cost increases net income, which is a direct poverty-reduction mechanism.

The third contribution is mechanization. Small farmers cannot individually afford tractors, harvesters, planters, laser land levellers, rice transplanters, threshers or silage machines. Cooperative machinery pools can provide shared access. This is important because poverty in agriculture is not caused only by land shortage; it is also caused by low productivity. Timely sowing, efficient harvesting, water saving and reduced labour bottlenecks increase yields and income. However, cooperative machinery centres must be well-managed. Recent evidence from Punjab’s crop-residue machinery experience in Indian Punjab shows that custom hiring centres can fail when they do not provide timely service, are understaffed or poorly maintained. Pakistan must learn from such experiences and design cooperative machinery services professionally.

The fourth role is marketing. The poor often remain poor because they sell cheaply and buy expensively. A farmer sells wheat, milk, vegetables or cotton immediately after harvest because he needs cash and lacks storage. Middlemen benefit from his weakness. Cooperative marketing societies can help members grade, store, process, transport and sell collectively. They can negotiate with mills, exporters, supermarkets and government procurement agencies. If farmers receive a better share of the final price, rural poverty declines without relying on subsidies.

Dairy cooperatives are especially relevant for Pakistan. Livestock is the largest component of agriculture, and millions of rural households own animals. Women are deeply involved in feeding, milking and caring for livestock. Yet milk markets are often dominated by collectors and middlemen. A dairy cooperative can collect milk daily, test quality, chill it, process it and sell it under a collective brand. This model has transformed rural economies elsewhere. India’s Amul is the most famous example. Reuters reported in 2025 that Amul is owned by 3.6 million Indian farmers, showing how dairy cooperatives can connect small producers to a large formal market. Pakistan, with its large livestock economy, can develop similar cooperative dairy systems in Punjab, Sindh and Khyber Pakhtunkhwa.

Women’s cooperatives can directly reduce household poverty. In rural Pakistan, women contribute to livestock, kitchen gardening, seed cleaning, embroidery, food processing, poultry, handicrafts and informal trade, but their work is often unpaid or underpaid. Women also face restrictions on mobility, finance and market access. A women’s cooperative can provide savings, small loans, training, collective marketing and social support. Such cooperatives can help women sell dairy products, stitched clothes, handicrafts, pickles, poultry, vegetables or processed foods. When women earn income, household nutrition, children’s education and health spending often improve.

Youth employment is another area. Pakistan’s youth bulge can become a demographic dividend only if young people find productive work. Rural youth often migrate to cities because villages lack enterprise. Modern cooperatives can create jobs in digital bookkeeping, input delivery, machinery services, milk collection, cold storage, e-commerce, transport, solar maintenance, seed production and food processing. A cooperative is not only an old rural credit society; it can be a modern rural enterprise platform.

Cooperatives also contribute to food security. Food security depends on production, access, affordability and stability. Farmer cooperatives can improve production through inputs and technology. Marketing cooperatives can reduce post-harvest losses. Dairy cooperatives can improve milk supply. Seed cooperatives can distribute better varieties. Storage cooperatives can prevent distress sales and stabilize prices. In Pakistan, where food inflation hurts the poor most, cooperatives can reduce both rural poverty and consumer vulnerability.

Climate resilience is now central to poverty alleviation. Floods, heatwaves, droughts and pests repeatedly push rural households into poverty. The World Bank has emphasized that Pakistan’s poverty reduction reversed partly because climate shocks such as the floods of 2022 and 2025 damaged livelihoods. Cooperatives can help poor communities adapt by sharing weather information, pooling crop insurance, managing water, storing seeds, protecting livestock, arranging emergency funds and supporting recovery after disasters. Climate adaptation is more affordable when communities organize collectively.

Water-user cooperatives can also play an important role. Pakistan’s agriculture depends heavily on irrigation, but water distribution is often unequal and inefficient. Tail-end farmers may receive less water. Watercourses may be poorly maintained. Conflicts over turns are common. Water-user associations and irrigation cooperatives can help maintain watercourses, schedule water turns, reduce waste and adopt efficient irrigation. Since water scarcity is becoming a major threat to food security and rural income, cooperative water governance is essential.

Savings cooperatives and credit unions can improve financial inclusion. Poor households often save informally through livestock, gold, rotating committees or cash at home. These methods are insecure and unproductive. Cooperative savings institutions can mobilize small savings and convert them into local lending. This reduces dependence on moneylenders and creates community-owned capital. However, financial cooperatives require strict auditing, professional management and member education; otherwise, fraud can destroy trust.

Housing cooperatives can also reduce urban and peri-urban poverty if properly regulated. Low-income families need secure land and affordable housing. Cooperative housing can reduce costs by pooling resources and acquiring land collectively. However, Pakistan’s housing cooperative sector has also suffered from fraud, overselling and weak oversight. Therefore, housing cooperatives can alleviate poverty only when land title, approvals, membership and finances are transparent.

The global community recognizes the poverty-reduction role of cooperatives. The United Nations declared 2025 as the International Year of Cooperatives under the theme “Cooperatives Build a Better World.” COPAC notes that the year highlights cooperatives’ role in addressing global challenges and advancing the Sustainable Development Goals. UN DESA states that the International Year is intended to raise awareness of cooperative enterprises’ contributions to poverty reduction, employment generation and social integration. This global recognition strengthens the argument that cooperatives are not outdated institutions; they are relevant to modern inclusive development.

Academic and book literature also supports this view. Johnston Birchall’s ILO book Rediscovering the Cooperative Advantage: Poverty Reduction through Self-Help argues that cooperatives can reduce poverty by giving poor people collective ownership, voice and economic participation. Birchall’s later work Cooperatives and the Millennium Development Goals also links cooperatives with poverty reduction, food security and community development. In the Pakistani context, K. Mustafa’s article “Cooperatives and Development” cites important works such as Agricultural Cooperative Movement in Pakistan: Perspective, Problems and Plan of Action by the Centre for Administrative Research and Development, and Chaudhry and Rizwani’s Role of Cooperative Institutions in Planned Change in West Pakistan. These references show that cooperative development has long been part of serious development scholarship.

Punjab’s cooperative sector shows both potential and weakness. A 2025 report in The Nation stated that Punjab had 32,792 cooperative societies, 1.71 million members, and working capital of about Rs 29.138 billion. These figures indicate a large institutional base. If even a fraction of these societies become active, transparent and development-oriented, they can support rural credit, input supply, machinery access, dairy development, women’s enterprise and local employment. But if they remain dormant, politicized or poorly managed, the sector will remain a missed opportunity.

Why have cooperatives underperformed in Pakistan? The first reason is elite capture. In many villages, powerful landowners, politically connected individuals or dominant families control institutions that are supposed to serve ordinary members. Poor farmers may remain members only on paper. Cooperative elections may be manipulated. Loans may go to influential people. Benefits may not reach the poorest. When the powerful capture cooperative institutions, the poor lose trust.

The second reason is politicization. Cooperative societies are supposed to be member-owned and autonomous. But political interference in lending, appointments, recoveries and leadership weakens them. When loans are treated as political favours rather than repayable credit, financial discipline collapses. When recoveries are not enforced equally, honest members suffer. A cooperative without discipline becomes a subsidy club, not a poverty-reduction institution.

The third reason is weak auditing. Trust is the heart of cooperation. If members do not know where money goes, they stop participating. Delayed audits, poor bookkeeping, cash-based records and lack of transparency create corruption. Digital records, independent audits and member access to accounts are essential. Without them, cooperatives cannot mobilize savings or attract credit.

The fourth reason is poor professional management. A modern cooperative must compete in markets. It needs bookkeeping, procurement, marketing, quality control, logistics, digital payments, inventory management and legal compliance. Many Pakistani cooperatives rely on untrained office bearers. Good intentions cannot replace professional capacity. Cooperative managers need training institutions and certification.

The fifth reason is limited awareness. Many members do not understand their rights. They do not attend meetings, read accounts or question leadership. Some people think a cooperative is a government department created to distribute loans or subsidies. This misunderstanding damages the cooperative spirit. Members must be educated that a cooperative is their own institution and that democratic participation is necessary for success.

The sixth reason is loss of public trust due to fraud. Housing cooperatives, credit societies and some agricultural cooperatives have sometimes been associated with mismanagement. When people lose money, the reputation of the whole cooperative sector suffers. This is why reform must include strict penalties for fraud and protection of honest members.

A counterargument is that cooperatives often fail and private markets are more efficient. Critics argue that cooperatives become slow, politicized and corrupt. They say private firms provide services more efficiently because they are driven by profit. This criticism has some validity in Pakistan’s experience. Many cooperatives have failed to deliver. However, the conclusion should not be that cooperatives are useless. The correct conclusion is that badly governed cooperatives fail, just as badly governed state institutions and monopolistic private markets fail.

Private markets are not automatically fair to the poor. A middleman may be efficient, but he may also exploit. A bank may be professional, but it may exclude small farmers. A private dairy company may collect milk, but it may pay low prices to producers. Cooperatives offer a different model: efficiency with member ownership. The challenge is to make them professionally managed, not to abandon them.

For Pakistan, a cooperative revival requires serious reform. First, cooperative laws should be updated to reflect modern economic realities while preserving democratic principles. Second, all cooperative societies should maintain digital membership records, loan records, asset registers, meeting minutes and audited accounts. Third, annual audits should be mandatory and accessible to members. Fourth, elections should be transparent, regular and protected from elite manipulation. Fifth, women, tenants, small farmers and youth should be included meaningfully.

Sixth, cooperative credit must be linked with savings and repayment discipline. It should not become politically influenced loan distribution. Seventh, the government should create credit lines for well-governed cooperatives, especially in dairy, machinery, storage, climate-smart agriculture and women’s enterprise. Eighth, cooperative training institutes should be strengthened. Ninth, digital payments should be used to reduce leakages. Tenth, provincial cooperative departments should shift from mere registration to development, monitoring and capacity building.

Punjab should lead this reform. Its large cooperative base, agricultural importance and rural population make it the natural centre for cooperative revival. The province should classify societies as active, inactive, dormant, fraudulent or reformable. Dormant societies should be merged or closed. Active societies should receive technical support. Fraudulent societies should face legal action. Dairy cooperatives, machinery cooperatives, seed cooperatives, water-user groups and women’s cooperatives should become priorities.

Pakistan should also connect cooperatives with poverty programmes. BISP beneficiaries, small farmers, rural women and youth skill programmes can be linked with cooperative enterprise models. Instead of giving only cash transfers, the state can help poor households build income-generating groups. Social protection and cooperative development should work together: cash support for survival, cooperatives for upward mobility.

Digital cooperatives are the future. A modern cooperative can use mobile apps for member records, online voting, market prices, input orders, machinery booking, milk payments and savings accounts. This can attract youth and reduce corruption. Pakistan’s growing mobile connectivity should be used to modernize rural cooperation.

The role of banks, universities and NGOs is also important. Banks can finance transparent cooperatives. Agricultural universities can provide technical support. NGOs can train women’s groups. Provincial departments can regulate and guide. The private sector can buy from cooperatives through contract arrangements. Cooperatives should not be isolated; they should be linked to the wider economy.

In conclusion, cooperative societies can play a major role in poverty alleviation in Pakistan because poverty is not only a problem of income; it is a problem of power, access and organization. Poor farmers, women, artisans, livestock owners and rural youth remain weak when they act alone. Cooperatives allow them to pool resources, reduce costs, access credit, improve bargaining power, enter markets, manage risk and build community assets.

Pakistan’s poverty challenge is serious, and recent World Bank reporting shows that earlier poverty reduction has reversed under the pressure of weak growth, inflation, structural weaknesses and climate shocks. Agriculture remains central to rural livelihoods, while livestock continues to be a major contributor to agriculture and GDP. In this context, cooperatives are not a romantic idea from the past; they are a practical necessity for inclusive development.

However, cooperatives will not automatically reduce poverty. They must be honest, democratic, professionally managed and digitally transparent. Pakistan’s cooperative movement has suffered from elite capture, politicization, weak audits, poor management and loss of trust. These weaknesses must be confronted directly. The cooperative principle has not failed; governance has failed.

The final lesson is clear: poverty cannot be defeated by charity alone; it must be defeated by organized economic power. Cooperative societies provide that power. If Pakistan reforms and modernizes them, they can become engines of rural development, women’s empowerment, food security, youth employment and poverty alleviation. If neglected, they will remain dormant institutions with unrealized potential. The choice before Pakistan is therefore between cooperative decline and cooperative renewal. For a country struggling with poverty, inequality and rural vulnerability, renewal is not merely desirable; it is essential.

The Indus Odyssey from Debal to Islamabad

The Ultimate Guide to Pakistan Affairs (711-2025). A focused Kindle guide for CSS, PMS, PCS, PPSC and FPSC Pakistan Affairs preparation.