- CSS Physics Paper-II 2026 Solved

- CSS Physics Paper-II 2025 Solved

- CSS Physics Paper-II 2024 Solved

- CSS Physics Paper-II 2023 Solved

- CSS Physics Paper-II 2021 Solved

CSS Essay Outline

- Introduction: accountability as the soul of cooperative democracy

- Thesis statement

- Meaning of cooperative societies

- Meaning of audit in cooperative societies

- Meaning of inspection in cooperative societies

- Difference between audit and inspection

- Why accountability is central to cooperatives

- Cooperative principles and democratic member control

- Historical background of cooperatives in South Asia

- Cooperative Credit Societies Act, 1904, and the origin of credit discipline

- Cooperative Societies Act, 1925, and legal accountability

- Pakistan’s cooperative sector and its development potential

- Punjab’s cooperative sector: scale, members and working capital

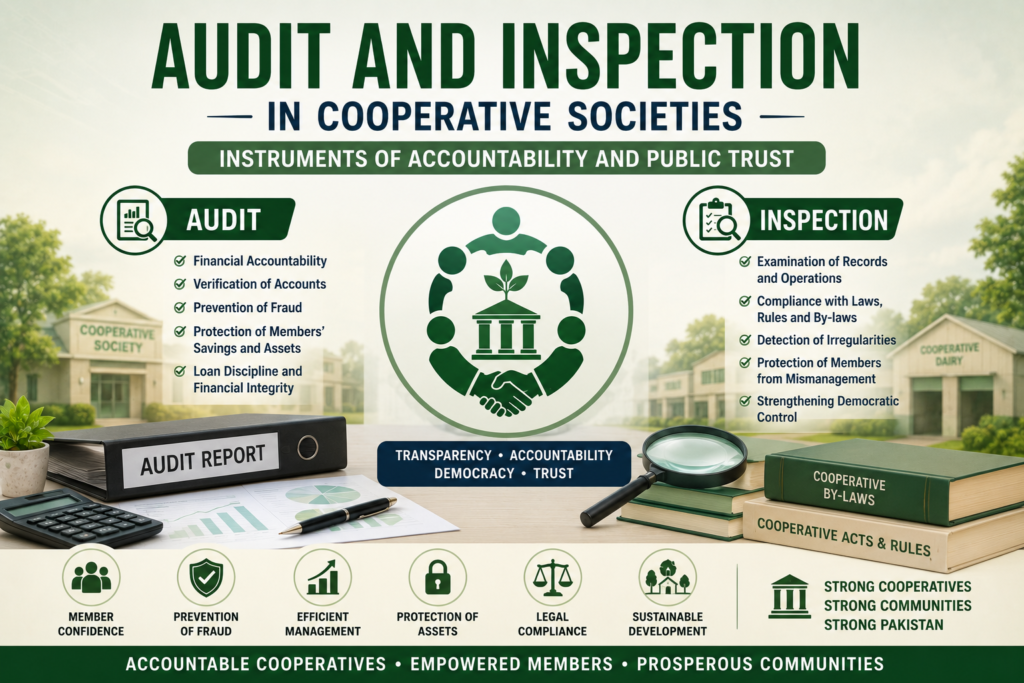

- Audit as financial accountability

- Audit as protection of members’ savings and assets

- Audit and verification of cash, securities, debts and liabilities

- Audit and prevention of fraud, embezzlement and misappropriation

- Audit and loan discipline in cooperative credit societies

- Audit and housing cooperative transparency

- Audit and member confidence

- Inspection as administrative and operational accountability

- Inspection and verification of society records

- Inspection and detection of illegal decisions by management committees

- Inspection and protection of ordinary members from elite capture

- Inspection and compliance with cooperative laws, rules and by-laws

- Role of Registrar Cooperative Societies

- Role of Chief Auditor and audit staff

- Audit and inspection in Punjab’s cooperative governance

- Cooperative frauds and the crisis of public trust

- Housing cooperatives, file fraud and weak oversight

- Why audit often fails in practice

- Why inspection often becomes routine rather than corrective

- Political interference and elite capture

- Lack of professional capacity and digital systems

- Delayed audits and outdated manual recordkeeping

- International standards and cooperative identity

- Book references: Birchall, ICA literature and Pakistani cooperative studies

- Counterargument: excessive audit and inspection may discourage cooperative autonomy

- Response: accountability protects autonomy; it does not destroy it

- Reform agenda: digital audit, risk-based inspection and public disclosure

- Policy recommendations for Pakistan and Punjab

- Conclusion: cooperatives can survive only where accountability is institutionalized

Essay

Cooperative societies are built on trust. They collect members’ savings, manage common assets, distribute loans, provide housing plots, supply agricultural inputs, market produce, run dairy systems, operate credit institutions, and sometimes manage land worth billions of rupees. In theory, a cooperative is one of the most democratic forms of economic organization because its members are both owners and beneficiaries. In practice, however, this democratic promise can collapse when records are manipulated, funds are misused, loans are distributed politically, plots are oversold, elections are controlled by elites, and ordinary members are denied access to information. Therefore, audit and inspection are not minor administrative exercises in cooperatives. They are instruments of accountability, transparency, and public trust.

The importance of audit and inspection becomes even greater in Pakistan, where cooperative societies have historically served farmers, housing members, small savers, rural communities, and middle-class families. The cooperative movement entered South Asia to protect agriculturists from exploitative credit systems and to promote thrift, self-help, and mutual aid. But over time, many cooperative institutions in Pakistan suffered from politicization, weak audits, elite capture, poor recordkeeping, and loss of public confidence. A cooperative without accountability becomes worse than an ordinary business because it exploits the language of community while betraying the trust of members.

The thesis of this essay is that audit and inspection are essential instruments of accountability in cooperative societies because they protect members’ money, verify records, detect fraud, enforce legal compliance, strengthen democratic control, and restore public trust. However, in Pakistan, especially Punjab, their effectiveness has been weakened by delayed audits, manual records, political interference, weak enforcement, lack of professional capacity, and elite capture. Therefore, Pakistan must modernize cooperative accountability through digital audit systems, risk-based inspections, independent professional review, public disclosure, member education, strict penalties, and transparent regulatory oversight.

A cooperative society is an autonomous association of persons who voluntarily unite to meet common economic, social, and cultural needs through a jointly owned and democratically controlled enterprise. The Punjab Cooperatives Department defines a cooperative in similar terms as an autonomous association of persons voluntarily cooperating for mutual social, economic, and cultural benefit. This definition highlights two key ideas: common benefit and democratic control. If either is lost, the cooperative loses its identity.

Audit in a cooperative society means the systematic examination of its accounts, financial transactions, cash balances, securities, loans, liabilities, assets, income, expenditure, and compliance with financial rules. It answers questions such as the following: Where did the money come from? Where was it spent? Were loans properly approved? Were recoveries made? Do cash balances match records? Were society funds used for societal purposes? Were assets protected? Were members informed? An audit is therefore the financial conscience of a cooperative.

Inspection is broader in some respects. It examines the working, management, records, decisions, membership, elections, meetings, by-laws, land matters, loan procedures, development work, and general functioning of a society. It answers questions such as the following: Is the management committee acting lawfully? Are records updated? Are members being denied rights? Are meetings held? Are by-laws followed? Is the society operating within its approved objectives? Are office bearers misusing authority? Inspection is therefore the administrative and operational watchdog of a cooperative.

The difference between an audit and an inspection is important. An audit focuses mainly on accounts and financial correctness. Inspection focuses on the overall functioning and legal compliance of the society. An audit may detect missing cash, doubtful loans, irregular expenditures, or false balances. Inspection may detect fake memberships, illegal committee decisions, non-holding of meetings, violation of by-laws, misuse of land, irregular elections, or denial of members’ rights. Both are complementary. Audit protects money; inspection protects governance.

Accountability is central to cooperatives because cooperatives are based on democratic member control. The International Cooperative Alliance states that cooperatives are democratic organizations controlled by their members, who actively participate in setting policies and making decisions; elected representatives are accountable to the membership, and in primary cooperatives, members have equal voting rights on the principle of one member, one vote. This principle cannot function without transparent accounts and accessible records. Members cannot control what they cannot see. They cannot vote meaningfully if they are misinformed. They cannot hold office bearers accountable if audits and inspections are delayed or suppressed.

Historically, the cooperative movement in South Asia was born out of the need for rural accountability and credit discipline. The Punjab Cooperatives Department records that the cooperative movement was introduced by the British government through the Cooperative Credit Societies Act, 1904, mainly to rescue agriculturists from exploitative credit systems. The objective was not simply to create loan-giving institutions; it was to build self-help organizations where members could save, borrow, and repay through mutual responsibility. Such a model requires an audit from the beginning because credit without accountability becomes default, and default destroys the institution.

The Cooperative Societies Act, 1925, remains a foundational law for cooperative societies in several parts of Pakistan, with provincial adaptations. The Punjab version of the Act includes provisions relating to inspection of documents, updating of records, audit, and the power of the Registrar in relation to cooperative societies. The Sindh version of the Act explicitly states that an audit includes examination of overdue debts, verification of cash balance and securities, and valuation of assets and liabilities. These legal provisions show that an audit is not optional. It is a statutory requirement designed to protect members and the public.

Pakistan’s cooperative sector still has significant development potential. Cooperatives can support rural credit, agricultural inputs, machinery services, dairy development, housing, savings, women’s enterprise, and poverty alleviation. Globally, cooperatives are again receiving attention. The United Nations declared 2025 the International Year of Cooperatives under the theme “Cooperatives Build a Better World,” recognizing their role in sustainable development and the Sustainable Development Goals. Reuters reported in 2025 that more than three million cooperatives operate globally and employ about 10 percent of the global workforce, showing that cooperatives are major economic institutions, not outdated welfare bodies.

Punjab’s cooperative sector also remains numerically large. A 2025 report in The Nation stated that Punjab had 32,792 cooperative societies, 1.71 million members, and working capital of about Rs 29.138 billion. It also noted that despite this scale, the cooperative movement had become increasingly dormant and struggled to keep pace with changing economic dynamics. These figures demonstrate why audit and inspection matter. When millions of members and billions of rupees are involved, weak accountability is not a technical flaw; it is a public-interest danger.

An audit is the first instrument of financial accountability. In cooperative credit societies, audits check whether loans are issued according to rules, whether members are genuine, whether collateral or guarantees are valid, whether recoveries are recorded, whether overdue debts are identified, and whether society funds are safe. In the absence of an audit, influential members may obtain loans repeatedly while poorer members are excluded. Office bearers may manipulate records. Bad loans may be hidden. Losses may grow silently until the society collapses.

Audit also protects members’ savings. Many cooperatives collect deposits, share capital, subscriptions, development charges, or service fees from members. A poor farmer, a retired employee, or a middle-class family may contribute money with the belief that the cooperative will use it honestly. An audit verifies whether that money has been properly recorded and used. If audit is delayed for years, misappropriation becomes easier and recovery becomes harder. A timely audit is therefore cheaper than a late investigation.

In housing cooperatives, an audit has special importance because land and development funds involve large values. A housing cooperative may collect money for land purchase, development charges, road construction, sewerage, electricity, parks, mosques, graveyards, and public facilities. The audit must verify whether money collected from members was actually spent on approved purposes. It must examine payments to contractors, land acquisition costs, bank balances, development liabilities, and recoveries from members. In societies where plot files are issued without land, an audit can expose the gap between promises and assets.

The danger of weak oversight in housing societies is visible in recent reported cases. In November 2025, Profit by Pakistan Today reported a NAB Rawalpindi probe into Islamabad and Rawalpindi housing schemes, alleging that private and cooperative housing schemes had oversold about 91,000 plots, marketed 80,000 kanals without approval, and issued 20,000 memberships despite no land availability. In May 2026, Pakistan Today reported that NAB investigators had found nearly 36,000 allegedly illegal plot files in the Islamabad Cooperative Housing Society case, with financial irregularities exceeding Rs16 billion, while several suspects had been arrested. These allegations remain subject to legal process, but they highlight the kind of public damage that audits and inspections are supposed to prevent early.

Audit also improves member confidence. A cooperative cannot survive if members suspect theft or favoritism. When audited accounts are presented in the general body meeting, members can ask questions. They can compare income and expenditure. They can evaluate the performance of the management committee. They can demand corrective action. Thus, audit strengthens democracy inside the cooperative.

Inspection, meanwhile, is the instrument of administrative accountability. It examines whether the society is functioning according to laws, rules, and by-laws. It checks whether records are updated, meetings are held, elections are conducted properly, membership registers are accurate, resolutions are lawful, and committees are not exceeding their authority. This is especially important because many cooperative failures begin not with theft but with small governance violations: meetings are skipped, records are not updated, members are not informed, elections are manipulated, and decisions are taken secretly.

Inspection protects ordinary members from elite capture. In many villages and housing societies, powerful groups can dominate management committees. They may control information, delay elections, admit fake members, exclude critics, or misuse society assets. A proper inspection can identify whether democratic rights are being violated. Since cooperatives are based on one member, one vote, any manipulation of membership or elections strikes at the heart of cooperative identity.

Inspection also ensures compliance with bylaws. Every cooperative society has objectives and rules. A credit society should not function like a private finance company. A housing society should not sell land beyond approved capacity. A dairy cooperative should not misuse member payments. A farming cooperative should not divert assets to private use. Inspection checks whether a society remains within its authorized purpose.

The Registrar of Cooperative Societies plays a central role in this accountability framework. The Registrar is responsible for registration, supervision, regulation, dispute handling, and enforcement under cooperative laws. The Punjab Cooperatives Department’s official disclosures show that its administrative scope includes matters such as inquiries, audits and inspections, reports, arbitration, and legal cases. The existence of such functions shows that cooperative accountability is recognized institutionally. The challenge is not the absence of a framework; it is the quality of implementation.

The office of chief auditor is also significant. Punjab Cooperatives Department documents refer to the post of Chief Auditor, Cooperative Societies, Punjab, indicating a formal audit structure within cooperative administration. But institutional titles alone cannot guarantee accountability. The audit system must be sufficiently staffed, professionally trained, independent in practice, and technologically equipped.

Why, then, do audit and inspection often fail? The first reason is delay. If an audit is conducted years after transactions, it becomes less effective. Records may disappear, office bearers may change, bank accounts may be closed, and funds may be unrecoverable. The audit should be annual, timely, and linked to the general body meeting. A late audit is like a post-mortem; a timely audit is preventive medicine.

The second reason is manual recordkeeping. Many cooperative societies still rely on paper registers, handwritten ledgers, physical files, and informal receipts. Such systems are easy to manipulate and difficult to verify. Digital records, online member registers, bank-linked payment systems, and scanned documents can reduce fraud. If a society collects money digitally and records transactions in real time, auditing becomes faster and more reliable.

The third reason is weak professional capacity. Cooperative audits require knowledge of accounting, law, land records, loan procedures, procurement, banking, and member rights. A poorly trained auditor may check arithmetic but miss structural fraud. A good auditor must identify irregular patterns: repeated loans to the same group, suspicious land payments, inflated contractor bills, unpaid dues of influential members, missing vouchers, fake memberships, or unexplained delays in possession.

The fourth reason is political interference. Cooperative societies often operate in local power networks. Politicians, influential landowners, developers, and pressure groups may influence management and regulators. If auditors and inspectors are pressured to ignore irregularities, accountability collapses. For audits and inspections to work, officers must have legal protection, institutional independence, and consequences for negligence or collusion.

The fifth reason is lack of follow-up. An audit report may identify irregularities, but no corrective action follows. An inspection may expose violations, but penalties are delayed. If reports do not produce action, they become paperwork. Accountability requires the full chain: detection, reporting, hearing, recovery, penalty, reform, and public disclosure.

The sixth reason is member ignorance. Many members do not read audit reports, attend general body meetings, or understand their legal rights. This allows office bearers to dominate. Audit and inspection become truly powerful only when members use them. Cooperative education is therefore part of accountability. Members should know how to demand accounts, question irregularities, access records, and vote responsibly.

Book literature supports this understanding. Johnston Birchall’s ILO work Rediscovering the Cooperative Advantage: Poverty Reduction through Self-Help emphasizes that cooperatives are powerful because they combine economic participation with member ownership and self-help. But self-help requires internal accountability; otherwise, the cooperative loses its advantage. Birchall’s Cooperatives and the Millennium Development Goals also link cooperatives with poverty reduction and social development, but such impact depends on democratic governance and member participation. Pakistani cooperative scholarship has also long recognized governance weaknesses. K. Mustafa’s article “Cooperatives and Development” refers to earlier works such as Agricultural Cooperative Movement in Pakistan: Perspective, Problems, and Plan of Action and Role of Cooperative Institutions in Planned Change in West Pakistan, showing that institutional reform has been debated for decades.

International cooperative principles also support audit and inspection indirectly. The ICA principles include democratic member control, member economic participation, autonomy, education, and concern for community. Audit supports member economic participation by showing how funds are used. Inspection supports democratic control by ensuring lawful governance. Education supports members’ ability to understand audit reports. Concern for community requires that cooperative assets not be misused by a few.

A counterargument is that excessive auditing and inspection may reduce cooperative autonomy. Cooperatives are supposed to be self-governing institutions, not bureaucratic departments. Too much interference by government officials can delay decisions, discourage innovation, increase corruption, and make cooperatives dependent on regulators. This criticism is valid in contexts where inspection becomes harassment or an audit becomes a fee-collecting ritual. A cooperative should not be suffocated by bureaucracy.

However, accountability does not destroy autonomy; it protects it. Autonomy without transparency becomes private control by office bearers. Democratic control without an audit becomes blind trust. Member ownership without inspection becomes vulnerable to capture. The correct approach is not to weaken audit and inspection but to modernize them. Regulation should be risk-based, transparent, time-bound, and professional. Honest societies should face minimal harassment, while high-risk societies should receive strict scrutiny.

The reform agenda should begin with a digital audit. Every cooperative should maintain digital accounts, member registers, loan ledgers, asset registers, meeting minutes, and bank reconciliation statements. Payments should move through banking channels wherever possible. Cash transactions should be limited. Audit software can flag unusual patterns such as repeated loans to connected persons, delayed recoveries, unexplained withdrawals, or mismatches between member contributions and assets.

Second, inspection should become risk-based. Societies with large funds, housing assets, repeated complaints, delayed audits, high default rates, or rapid membership growth should be inspected more frequently. Small, compliant societies should not be burdened unnecessarily. Risk-based inspection improves efficiency and reduces harassment.

Third, audit reports should be disclosed to members. Every member should have the right to access audited accounts, inspection summaries, and compliance status. Societies should display key financial information at their offices and through online portals. Transparency is the best disinfectant.

Fourth, audit objections must be time-bound. If an audit identifies irregularities, the management committee should respond within a fixed period. The registrar should decide the matter within a reasonable timeframe. Recoveries and penalties should not remain pending indefinitely. Delayed accountability encourages wrongdoing.

Fifth, cooperative auditors and inspectors should receive specialized training. They should understand cooperative law, accounting standards, fraud detection, land records, digital systems, procurement rules, and member rights. Professional certification should be introduced for cooperative auditors.

Sixth, external audits should be used for large societies. Small societies may be audited through departmental systems, but large housing, credit, dairy, or multi-purpose societies should undergo professional external audits by qualified auditors, alongside statutory cooperative audits. This will improve credibility.

Seventh, member education should be mandatory. Cooperative departments should train members to read basic financial statements, understand audit reports, participate in meetings, and elect responsible committees. A silent membership is an invitation to capture.

Eighth, penalties must be strict. Office bearers who embezzle funds, issue fake files, manipulate memberships, hide records, or obstruct audits should face removal, recovery, disqualification, and criminal proceedings where necessary. Accountability without consequences is decoration.

Ninth, cooperative regulation should protect whistleblowers. Members, employees, or auditors who report fraud should not be victimized. Anonymous complaint systems and legal protection can help expose irregularities early.

Tenth, Punjab should create a real-time cooperative accountability dashboard. Since Punjab has tens of thousands of societies and more than a million members, manual supervision is insufficient. The dashboard should show audit status, inspection status, elections, complaints, pending inquiries, recoveries, and legal cases. Public categories may include compliant, delayed audit, under inspection, under inquiry, and suspended. Such transparency would create pressure for compliance.

The importance of such reform is greater after the UN’s International Year of Cooperatives 2025. The theme “Cooperatives Build a Better World” is inspiring, but cooperatives can build a better world only if they are themselves accountable. A corrupt cooperative does not build community; it destroys it. A transparent cooperative, on the other hand, can reduce poverty, support agriculture, provide housing, empower women, and strengthen local democracy.

In conclusion, audit and inspection are not technical formalities in cooperative societies. They are the instruments through which cooperative democracy becomes real. An audit protects money, verifies accounts, identifies fraud, and strengthens member confidence. Inspection protects governance, enforces law, checks records, and prevents elite capture. Together, they preserve the cooperative identity of self-help, mutual aid, and democratic ownership.

Pakistan’s cooperative sector, especially in Punjab, has large potential but serious trust deficits. With more than 32,000 cooperative societies and 1.71 million members in Punjab alone, accountability cannot be left to paper registers and delayed inspections. The reported scale of housing-society irregularities in Islamabad and Rawalpindi shows that weak oversight can cause massive public harm. Audits and inspections must, therefore, become preventive, digital, professional, and member-centered.

The final lesson is clear: a cooperative without accountability is cooperation in name only. If Pakistan wants cooperatives to reduce poverty, support farmers, provide housing, and strengthen rural development, it must first protect members from fraud and mismanagement. Audit and inspection are the eyes and ears of cooperative accountability. When they are strong, cooperatives become engines of trust. When they are weak, cooperatives become vehicles of exploitation. The future of Pakistan’s cooperative movement will depend not only on registration and membership but also on whether every rupee, every record, every decision, and every office bearer can be held accountable before the members.

The Indus Odyssey from Debal to Islamabad

The Ultimate Guide to Pakistan Affairs (711-2025). A focused Kindle guide for CSS, PMS, PCS, PPSC and FPSC Pakistan Affairs preparation.